The Town of Newmarket's primary funding source is property tax which is divided between the Town of Newmarket, York Region and the school boards. Property taxes enable the Town to provide the high quality of municipal programs and services that Newmarket residents are accustomed to.

Newmarket determines your property taxes by multiplying your current value assessment (determined by the MPAC) by the Town's tax rate, the Region of York's tax rate and the provincial education tax rate.

Note: Please contact our office before the instalment due date(s) if you don’t receive a tax bill. Failure to receive a tax bill or notice does not excuse a taxpayer from the responsibility for payment of the taxes nor relieve the liability for Penalty/Interest.

On this page

Property tax portal coming soon!

A new online property tax portal is coming soon!

With the online tax portal, property owners can access their tax information online, anytime. The portal will allow property owners to view account information, print tax statements, check their balance and more!

Check back on this webpage for more information on how to register for an account once the portal is launched.

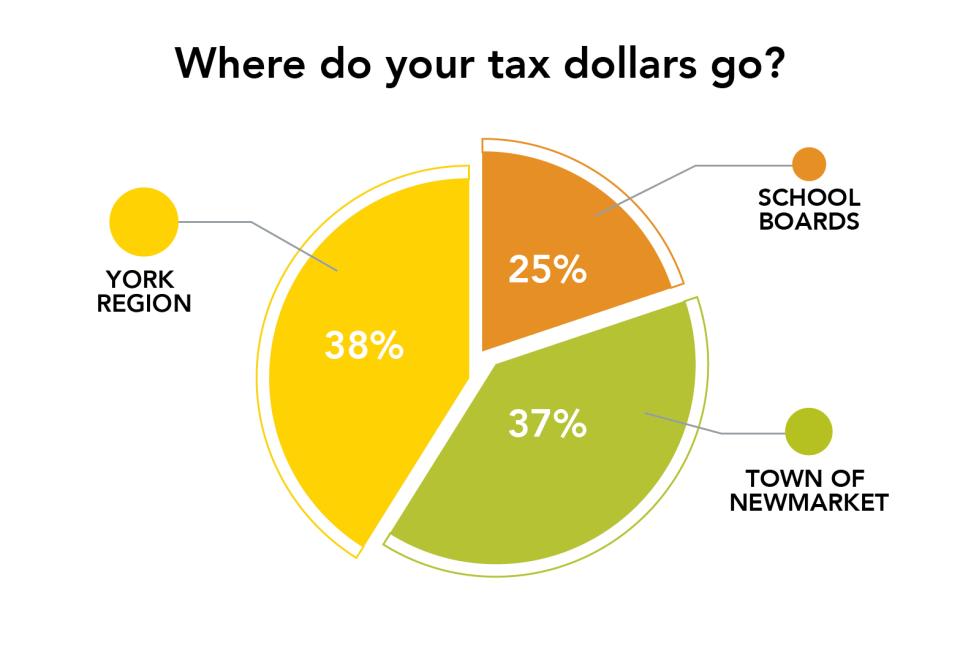

Where do property taxes go?

Image

Breakdown of where your taxes go

Property tax increases

Glossary of tax terms

AboutMyPropertyTM is a secure, online service that provides property owners with convenient access to basic property valuation information. Through AboutMyPropertyTM, all property owners have access to their assessment roll information (e.g. current value assessment, legal discretion, lot size) and assessment roll values on comparable properties of their choice.

The law that governs the way property is assessed for taxation purposes in Ontario.

The four year cycle of assessment-related activity which leads to the delivery of revised current value assessments to municipalities for taxation purposes for the next four years.

An independent tribunal, which reports to the Ontario Ministry of the Attorney General and hears assessment appeals from property taxpayers.

The value of a property (land and buildings) for taxation purposes.

Capping refers to a municipality’s option to limit, or cap, the tax increases on commercial, industrial and multi-residential properties only. A limit on tax decreases, to fund the cost of capping, is known as a clawback.

The price a property might reasonably be expected to sell for on the open market, by a willing buyer from a willing seller, in an arm’s length transaction. For property assessment purposes, current value and assessed value are the same thing.

Property which is assessed, but not taxed. Generally, properties which are exempt from property taxes provide services for the public good, such as schools, churches and hospitals, along with government locations. Other charities and philanthropic organizations mentioned in the Assessment Act may be given exempt status if certain criteria are met. Properties eligible for exemption are found in Section 3 of the Assessment Act.

The statute governing all aspects of municipal operations, including the levy and collection of property taxes and the addition of penalty and interest charges.

The process of collecting information in a municipality for the purposes of preparing preliminary voters’ lists for municipal and school board elections, lists of potential jurors and the Ontario Population Report. MPAC carries out an enumeration every four years in the same year as municipal elections.

An assessment which has not been recorded on the assessment roll. When an omitted assessment is added to the assessment roll, property taxes can be collected for the current year and, if applicable, for any part or all of the previous two years.

Payments made to municipalities by the provincial or federal government, where properties are exempt from property taxation.

A notice sent to all property owners every four years (reassessment years) to advise them of their property's current value assessment. The Notice also contains the property's classification and school support designation. Notices may also be received in any year where changes have occurred to the property.

MPAC’s staff who determine current value assessments for properties in Ontario.

The categorization of a property according to its use, used for tax class purposes. There are seven major classes of property: residential, multi-residential, commercial, industrial, pipe line, farm or managed forest.

The combined tax for a property comprising the municipal (local) levy, the regional levy and an education levy.

The process of updating assessments on all properties in Ontario to reflect more current values. This is done every four years. The most recent was January 1, 2016.

Due to the COVID-19 pandemic, the Ontario government postponed the 2020 Assessment Update. On August 16, 2023, the Ontario government filed a regulation to amend the Assessment Act, extending the postponement of a province-wide reassessment through the end of the 2021-2024 assessment cycle.

A designation from an individual which enables that person to elect school trustees and direct property taxes to that Board.

An assessment made during a taxation year for an addition, renovation or construction as well as a change in classification. When a supplementary assessment is added to the assessment roll, additional property taxes can be collected for that portion of the current tax year that the supplementary addresses.

The annual amount of property tax in dollars, which is paid by the Town’s taxpayers – residential, commercial and industrial.

The amount by which the Tax Levy must be increased to balance the budget. This is close to, but not the same as, the increase for the average residential taxpayer.

A percentage applied to the assessed value of a property to determine property taxes payable. Municipal tax rates are set by local municipalities (both local and regional) and education tax rates are set by the provincial government. Tax rates may differ for each property class.

The calendar year (January 1st to December 31st).

A fixed point in time on which current assessment values are based. This date is set by the provincial government. The valuation date in Ontario is January 1st.